Omnis 4th December

Posted by Nigel on Monday 4th of December 2023

Omnis Weekly Market Update – 4th December 2023

An overall mixed week for markets, with three of the five major indexes seeing positive returns. Cooling inflation data has been welcomed by investors in the world’s major economies, as expectations of interest rates being cut in 2024 continue to grow. In the U.S., new unemployment data proved helpful to the central bank’s goal of a soft economic landing.

Last week’s performance – major stock markets

|

S&P 500 |

+0.77% |

|

Nikkei 225 |

-0.58% |

|

CSI 300 ... |

Autumn Statement

Posted by Nigel on Thursday 23rd of November 2023

The 2023 Autumn Statement: Winners and Losers

UK Chancellor Jeremy Hunt’s 2023 Autumn Statement outlined, in his words, “eight months of hard work” and no fewer than 110 measures to help grow the British economy. Contained within are a raft of measures set to overhaul everything from minimum wage and benefit payments to tax, business investment, and more.

The Winners

Young and low-paid staff

Although the news was released ahead of the main statement, the announcement confirmed a large-scale increase to the national living wage, bring...

OMNIS Nov 13

Posted by Nigel on Monday 13th of November 2023

A mixed week for markets, with four of the five major indexes seeing positive returns. Despite this, governments and central banks remain vigilant as weak economic activity persists in the world’s largest economies. The UK’s FTSE 100 was the only major index to see a decline, as the British economy stagnated in the third quarter of 2023.

Last week’s performance – major stock markets

|

S&P 500 |

+1.31% |

|

Nikkei 225 |

+1.93% |

|

CSI 300 |

+0.07% |

|

Euro Stoxx 50 |

+0.54% |

|

FTSE 100 ... |

Private Health

Posted by Nigel on Wednesday 8th of November 2023

Should I consider private medical insurance?

Life can be full of surprises. You can’t be prepared for everything. You may have some insurance to support you financially if the unexpected happens, but have you considered how private medical insurance might offer you and your family the peace of mind you need if your health takes a turn for the worst?

A growing trend

According to data published by The Telegraph, close to half a million people have taken out private medical insurance over the past year, as NHS waiting lists hit record l...

Interest rate

Posted by Nigel on Thursday 2nd of November 2023

The hold in the BoE rate at 5.25% was predicted in the markets and comes on the back of ECB (European) and Fed (US) rate holds.

In changing times, investors should keep a cool head and a well-diversified portfolio. Omnis spread your investments across different asset classes, global regions and styles which can smooth returns and reduce the risks to which you are exposed.

Staying Invested

Posted by Nigel on Thursday 26th of October 2023

Three Important Reasons for Staying Invested through Market Downturns

It’s been a difficult year for investors so far. Inflation and political uncertainty have led to market volatility. Market volatility can be scary, especially if the value of your investments drops, but it’s important not to let fear guide your decision about whether to stay invested in your portfolio.

Here are three reassuring reasons for staying invested in the stock market during uncertain times.

The best financial decisions are not based on emotion

Emotions c...

Cancelling Financial Protection

Posted by Nigel on Friday 20th of October 2023

Cancelling your financial protection during the cost of living crisis could be a bad idea

Centuries ago, Benjamin Franklin said that...

“By failing to prepare you are preparing to fail.”

This is especially true when it comes to ensuring your personal finances are protected from the rainiest of days. If the rising cost of living is likely putting pressure on your spending, you may be considering cancelling your cover, even when this could leave you more vulnerable than before. Read on to discover some of the reasons you should con...

Why Planning is Crucial!

Posted by Nigel on Wednesday 11th of October 2023

Making your retirement savings last a lifetime

To help ensure a sustainable income, you first need to understand how much you’ll need to live on.

• On the go – during the early stages of retirement, there’s a strong likelihood that you’ll spend more on travel, hobbies, or home improvements

• Slowing down – while you may be slightly less active, you’re still busy with hobbies, but you may be less inclined to long-haul travel

• Coming to a stop – in later life, your mobility may be more limited, which risks increasing costs due to needing care

Structuring a sustainable income

The most efficient retirement income strategy should be planned well in advance and ensure that:

• Allowances and exemptions are used to their full capacity

• Married couples plan together so income and assets are allocated effectively of Cost Living “You first need to understand how much you’ll need to live on.

“You first need to understand how much you’ll need to live on.”

When it comes to withdrawing funds, you may want to consider using cash first, followed by taxable investments, ISAs, and finally pensions.

Tax efficiency is key

While tax-efficient savings helps enhance your wealth for retiring in style, tax-efficient withdrawals helps preserve your capital and increases the chance of having money to leave to your loved ones.

So, maximise all your tax allowances including:

• Income Tax allowances

• The Dividend allowance

• 5% return of capital allowance from investment bonds

• Personal savings allowance

• ISA allowance

• Capital Gains Tax allowance

By planning together, couples can use these allowances to maximise the amount of tax-free income available.

Consider spending excess cash first

Ideally, you should hold an emergency fund to cover around six months of regular expenditure. If you have more cash available, consider using this before withdrawing from pensions. Using excess cash allows you to leave funds invested, which may provide enough time for funds to recover any lost value.

Think twice before drawing on your pension

While you may consider your pension as the foundation of your retirement plan, if you have other income that uses your tax allowances, it may be prudent to defer drawing on your pension. Since pension funds benefit from tax free growth, interest, and dividends, leaving your pension invested is especially useful for maintaining capital value. Plus, pension funds are usually not subject to IHT.

Leaving your pension fund intact while drawing on other investments may help to reduce your IHT liability.

Enjoy flexibility from ISA savings

ISAs are considerably more flexible than pensions. Growth, interest, and dividends are all free of tax and you can withdraw money tax-free without restriction. As for IHT, ISAs can be passed between spouses on death, which preserves the tax-efficient treatment.

Useful in reducing tax in retirement, you can use your ISA to:

• Fund large, one-off purchases

• Top up your income – especially useful if your pension exceeds your tax-free allowance

• Make your portfolio more efficient over time, by gradually moving taxable funds across

Take a savvy approach to investment accounts

A basic and flexible wrapper, investment accounts can hold funds, shares and investment trusts. Interest and dividends are taxable at your marginal rate and selling assets can incur Capital Gains Tax (CGT) if your profit exceeds your annual exemption (£6,000 for 2023/2024 or, for a couple, £12,000).

The following strategies can help reduce tax:

• Move your taxable investment accounts into ISAs

• Use your annual CGT exemption to avoid large gains rolling up

• Structure your investments depending on the type of income they generate

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Past performance is not a guide to future performance and should not be relied upon.

An ISA is a medium to long-term investment, which aims to increase the value of the money you invest for growth or income or both.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen. Tax concessions are not guaranteed and may change in the future. Tax free means the investor pays no tax.

Get in touch

If you’d like help to create a financial plan to structure a tax-efficient income in retirement, we can help. Please get in touch to arrange a time to chat.

Approved by The Openwork Partnership on 04.10.2023

Is now a good time to remortgage?

Posted by Nigel on Wednesday 27th of September 2023

Is now a good time to remortgage as the Bank of England base rate stays the same?

Whilst the Bank of England base rate remains the same, interest rates are still the highest they have been in 15 years. So, if you are one of the thousands coming to the end of your fixed rate deal over the next few months it’s very likely you’ll see your payments increase as a result of higher mortgage rates but it’s a common misunderstanding that the Bank of England base rate is directly linked to the mortgage rates on offer. There are many factors that d...

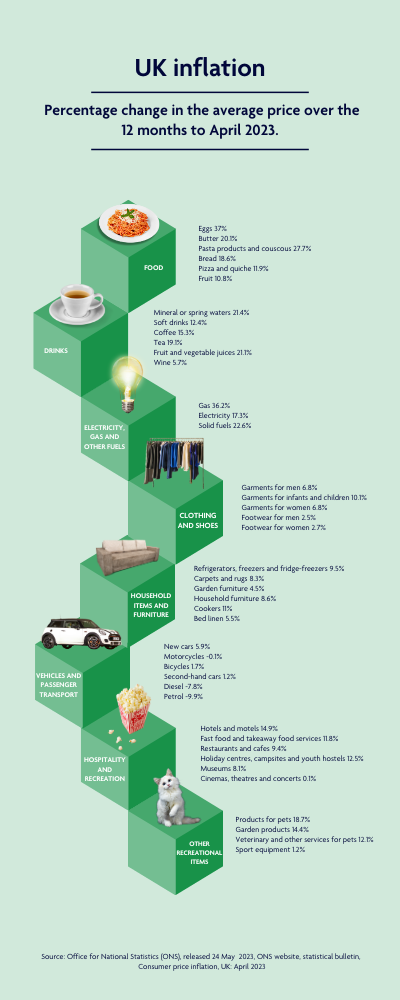

UK Inflation May 23

Posted by Nigel on Wednesday 31st of May 2023

Inflation and cost of living are two topics constantly on the tips of our tongues lately. The Openwork Partnership have put together the below infographic to show the changes from April ’22 to April ’23.