Omnis Weekly Update April 24th

Posted by Nigel on Monday 24th of April 2023.

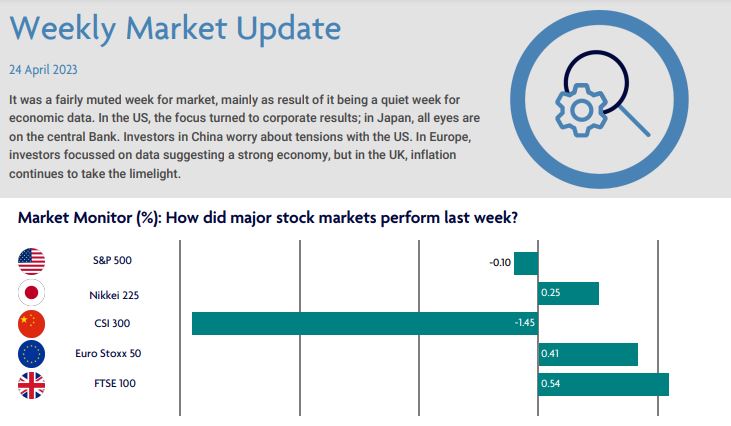

US: Focus turns to corporate results

It was a relatively light week in terms of economic data and therefore all eyes were on companies’ financial results for the first quarter of this year. So far company results appear to be better than expected. Data suggests that the labour market in the US is weakening. Is this good news or bad news? On one hand, is it good news because this could encourage the Federal Reserve to slow down, or even stop, hiking interest rates? On the other, could this weakening suggest a recession is around the corner?

Japan: Inflation pressures remain

Inflation in Japan sits at 3.1% putting pressure on the Bank of Japan. However, the Bank of Japan has reiterated their commitment to keeping policies very supportive of the economy, meaning low interest rates. In terms of economic activity, we continue to see weakness in the manufacturing sector due to suppressed global demand, but the services sector is picking up the slack due to the post-Covid reopening.

China: Economic data vs US investment curbs

The Chinese economy grew more than expected in the first three months of the year boosted by good export growth, infrastructure spending and a rebound in retail spending. Home prices are also rising at the fastest pace in almost two years following a few years of trouble for the sector. However, investor sentiment was dampened by signs that the U.S. may introduce fresh investment curbs against China.

Europe: A more resilient economy?

Stocks rose as optimism about the economic outlook outweighed concerns about interest rates staying higher for longer. Business activity in the Eurozone appears to have picked up in April and shows sign of expansion, particularly in the services sector, suggesting the economy is more resilient than expected. Investors expect the European Central Bank to continue raising interest rates as inflation remains elevated.

UK: Inflation remains uncomfortably high

Inflation in the UK remains in double digits at 10.1%, higher than many had expected and driven by surging food and drink prices. Further data showed signs that wage growth was still strong – investors are therefore expecting another interest rate hike from the Bank of England in May. In terms of economic activity, data suggest that whilst the manufacturing sector continues to decline, the services sector appears to be growing for the month of April.

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.