Should you pay a fee for your mortgage advice? Let us take you through the process.

Posted by Nigel on Wednesday 29th of March 2023.

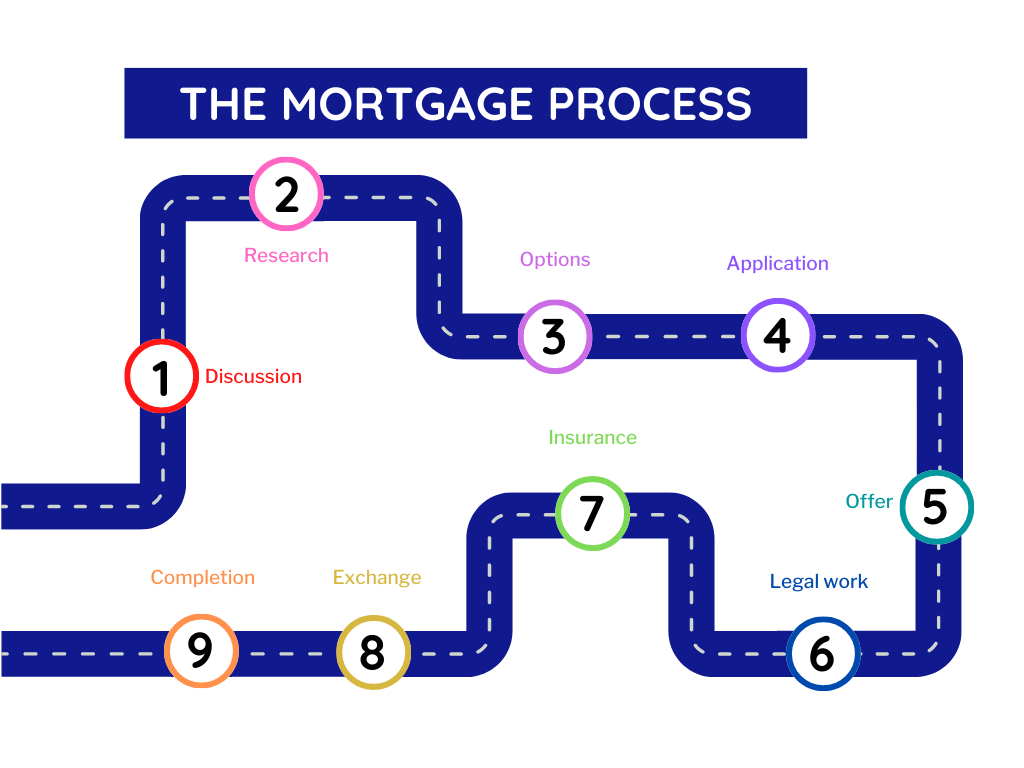

Looking at the image above it looks pretty straightforward, right? That’s the ideal scenario, though there can be some instances where you might need a bit of a hand hold. That’s where having a mortgage adviser to guide you through can be beneficial.

As an example let’s have a look at one of our more recent cases, Nathan and Jennifer, a young professional couple looking to purchase their first home.

We first spoke with Nathan back in the summer of 2022, when he was looking to potentially purchase a property by himself, with a helping hand in the form of a deposit from his father. While it was possible, after a discussion with his partner, Jennifer, they decided that their preferred approach would be to purchase their first home together.

After identifying a lender that accepted the gifted deposit, and took into account that Jennifer was new to her role the application was submitted in October.

Nathan and Jennifer borrowed £292,500 over 30 years at a rate of 5.9% fixed for five years. Though they could have had a longer overall term, the monthly payment of £1,758 fitted within their budget.

Now at this point, you’d think that that’s all there is to do, and to wait for the legal works to complete and pick up your keys in a few months’ time. Which is what you’d do if you arranged your mortgage directly with the lender.

As your adviser, it’s part of our role to keep an eye on rates and should a better rate, with the same lender, become available, we will investigate if you are able to switch to the new rate.

Later the same month, a new rate did become available, 5.49%, bringing the monthly payment down to £1,665 – a saving of £93 per month for Nathan and Jennifer.

Two months later, rates dropped again, to 5.08%, further reducing the monthly payment to £1,590 – a further saving of £75 per month.

The following month, a further reduction was announced, 4.49%, reducing the monthly payment to £1,384, another £206 saved. This was the last change to be made as exchange was scheduled for a week later.

Overall Nathan and Jennifer saved £374 per month, that’s £22,440 over the five year fixed term of their mortgage. To say they were happy is a bit of an understatement!

This is just one of the reasons it’s good to have a mortgage adviser in your corner during what is one of the more stressful moments in life.

Prior to informing clients of rate reductions, a new affordability calculation is carried out, and sense checked with our contact at the lender, agreement is always sought from the lender before approaching the client with the new rate.

YOUR HOME MAY BE REPOSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE

Approved by The Openwork Partnership 22/03/2023

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.